Finding the best mortgage interest rates in the UK is a priority for homebuyers and current homeowners alike. Given the high cost of property and extended repayment periods, even a slight difference in interest rates can mean significant savings over the loan term. With the housing market constantly shifting, securing a competitive interest rate has never been more important, as it directly impacts your monthly budget and overall financial health.

In this article, we’ll guide you through the current mortgage interest rates in the UK, breaking down everything you need to know about various rate types, recent trends, and how to choose the best mortgage product for your unique needs.

Table of Contents

Overview of Best Mortgage Interest Rates in the UK

What is a Mortgage Interest Rate?

A mortgage interest rate is the percentage a lender charges for borrowing funds to purchase a home. This rate is added to the principal mortgage amount and repaid over time through monthly installments. Mortgage interest rates in the UK significantly impact your monthly mortgage repayments and, ultimately, the total cost of the loan.

Types of Mortgage Rates

Understanding the types of mortgage rates is essential for choosing the best deal. There are several options available in the UK mortgage market:

- Fixed-Rate Mortgages: These mortgages come with a fixed interest rate for an agreed term, typically two, three, or five years. The main advantage is stability in monthly payments, regardless of market fluctuations. However, once the term ends, the mortgage usually reverts to the lender’s standard variable rate (SVR), which may be higher.

- Variable-Rate Mortgages: Variable-rate mortgages have an interest rate that fluctuates according to market conditions or the Bank of England’s base rate. This can make budgeting more challenging, as payments may rise if rates increase. However, borrowers may benefit when rates drop, reducing monthly payments.

- Tracker Mortgages: Tracker mortgages are a type of variable-rate mortgage that follows the Bank of England’s base rate plus a fixed margin. For instance, if the base rate is 1% and the lender charges a margin of 1%, your interest rate would be 2%. While tracker mortgages align with the central bank’s movements, they can lead to unpredictable monthly costs.

Factors Affecting UK Mortgage Rates

- Bank of England Base Rate: This central bank rate serves as a reference for lenders and significantly influences mortgage rates. If the Bank of England raises its base rate, mortgage rates generally follow, affecting new borrowers and those with variable or tracker mortgages.

- Lender Criteria and Personal Factors: Mortgage lenders assess your credit score, employment history, and financial background to determine your interest rate. A higher credit score and substantial deposit can help you access more favorable rates, as lenders view you as a less risky borrower.

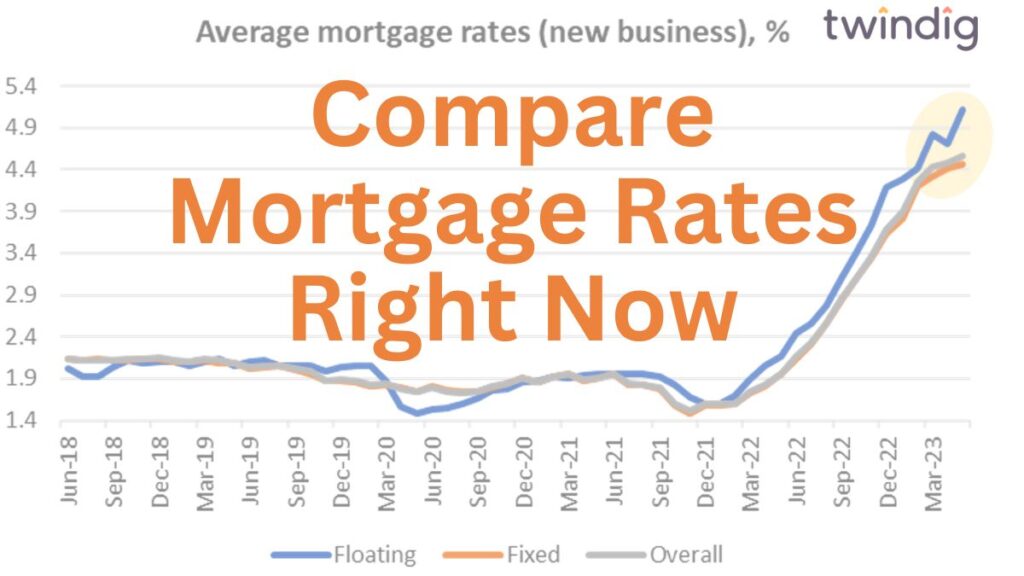

Why It’s Important to Compare Mortgage Rates Right Now

Current Market Trends

The UK mortgage market has experienced notable fluctuations recently. Rate increases have been prevalent, spurred by economic changes and adjustments by the Bank of England. In response to high inflation, the Bank of England has gradually increased its base rate, leading to higher mortgage rates overall. This trend impacts not only first-time buyers but also homeowners seeking to remortgage, making it crucial to compare options actively.

Impact of Inflation and Economic Policies

Inflation significantly influences mortgage rates, as higher inflation often prompts the Bank of England to raise the base rate to stabilize the economy. Additionally, government policies, including housing incentives or market interventions, can impact mortgage rates. Monitoring these changes can help you stay ahead and make well-informed decisions.

Potential Savings

Comparing mortgage rates can lead to substantial savings. For first-time buyers, securing a lower interest rate can make monthly payments more manageable, freeing up funds for other expenses. Homeowners considering remortgaging can also benefit by locking in a lower rate, reducing their monthly outgoings and overall loan costs. Even a 0.5% difference in interest rates can translate to significant savings over a typical 25-year mortgage.

Best Mortgage Rates Available Right Now

It’s essential to explore and compare the current offerings from various lenders to determine which option best suits your financial profile. As of now, leading UK lenders offer competitive rates across fixed, variable, and tracker mortgage products. Consider this example comparison:

| Lender | Product | Interest Rate (%) | Initial Term | APRC (%) |

| Lender A | Fixed (2 years) | 3.5 | 2 years | 4.2 |

| Lender B | Variable | 3.8 | No fixed term | 4.3 |

| Lender C | Tracker (BOE + 1%) | 2.75 | 2 years | 3.9 |

These rates are indicative and vary based on the borrower’s credit profile and the deposit amount. Always consult a mortgage broker or lender for the latest rates and terms that suit your circumstances.

How to Qualify for the Best Mortgage Rates

To secure the best rates, consider the following:

- Improve Your Credit Score: Lenders prefer borrowers with a good credit history, as it shows responsible financial behavior. Take time to check your credit report, clear any outstanding debts, and avoid large credit applications before applying.

- Save for a Larger Deposit: Lenders often offer lower rates to borrowers with larger deposits, as this reduces the loan-to-value (LTV) ratio. Aim for at least 20% to access more competitive rates, though higher deposits may yield even better options.

- Consider a Mortgage Broker: Mortgage brokers have access to various products, some of which are not publicly advertised. A broker can match you with the most suitable rates based on your financial profile and goals.

Tips for Securing the Right Mortgage in the UK

- Fixed vs. Variable Rate Considerations: Evaluate whether the stability of a fixed rate or the flexibility of a variable rate best fits your financial situation. Fixed rates provide security, while variable rates offer potential savings if market rates fall.

- Remortgaging for Better Rates: If your initial mortgage term is ending or you’re on an SVR, consider remortgaging to secure a lower rate. This can significantly reduce your monthly repayments and total interest over time.

- Locking in Rates at the Right Time: Given the current economic environment, locking in a fixed rate may be wise if you prefer stability. Some lenders offer a “rate lock,” allowing you to secure a rate before finalizing your mortgage.

Conclusion

Securing the best mortgage rate in the UK can lead to substantial financial benefits over the loan term. With today’s fluctuating market conditions, it’s crucial to stay informed, compare current rates, and assess which mortgage product aligns with your needs. For first-time buyers and current homeowners, navigating mortgage options can seem overwhelming, but by comparing rates and understanding the factors at play, you can make empowered decisions that safeguard your financial future.

Take Action: Speak with a mortgage advisor or broker to find the best rates tailored to your profile and lock in the savings available today.

FAQs

1. What is considered a good mortgage interest rate in the UK?

A good mortgage interest rate in the UK depends on market conditions and the type of mortgage you choose. Generally, a fixed-rate mortgage below 4% is considered competitive in today’s market. However, this can vary based on factors such as your credit score, deposit size, and the loan-to-value (LTV) ratio.

2. How often do mortgage interest rates change in the UK?

Mortgage interest rates can change frequently, especially if they are tied to the Bank of England base rate, which is reviewed monthly. Fixed-rate mortgages will remain constant during the fixed period, while variable and tracker rates may adjust based on changes to the base rate or other economic factors.

3. What type of mortgage rate is best: fixed, variable, or tracker?

The best type of mortgage rate depends on your financial goals and risk tolerance. Fixed rates offer stability and predictable payments, which can be ideal for long-term planning. Variable and tracker rates may fluctuate, providing potential savings when rates drop, but they can also increase, which may be better suited for those with more financial flexibility.

4. Can I negotiate my mortgage interest rate with lenders in the UK?

Yes, mortgage rates can sometimes be negotiated, especially if you have a strong financial profile, a high credit score, or a large deposit. Working with a mortgage broker can also help you access exclusive deals and potentially secure a more favorable rate than you might find independently.

5. Is it worth remortgaging to get a lower interest rate?

Remortgaging to a lower interest rate can be worth it, especially if you’re on a standard variable rate (SVR) or your initial fixed-rate period has ended. A lower rate could reduce your monthly payments and save you money over the loan term, but be sure to factor in any remortgage fees to determine if it’s cost-effective.

Mutual Funds: Types, Benefits, and How to Invest

Best stock market investment strategy

How do I apply for Social Security retirement benefits?

How to Start Investing with Little Money

How to Start the Best Value Investing Strategy

10 Tips to Improve Your Credit Score

The Best Index Fund and ETF in The Stock Market

How to set up a Monthly Budget Planner